With a wealth of experience and a keen eye for detail, we guide you through every step of the buying or selling process.

We are always happy to discuss conveyancing work at an initial meeting at no cost or obligation and a conveyancing quote setting out all of the fees and disbursements for you to consider.

You can get started today by obtaining a free, no obligation quote from Sydney Mitchell by clicking the link here.

Sydney Mitchell are on the panel of most high street banks and building societies. This means that when you are purchasing a property with the aid of a mortgage, we can also act on behalf of those lenders.

For confirmation of our panel membership with a specific mortgage lender, please contact our Shirley office on 0121 746 3300.

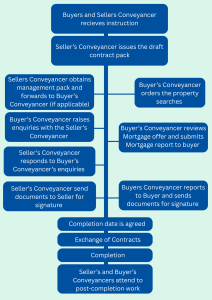

The process of buying and selling a residential property

Buying and selling a property can be quite an overwhelming and complicated process. Instructing an experienced conveyancer helps to simplify the transaction, as they will guide you through the process and deal with the legal matters for you.

Below is a step-by-step guide to the key steps in an average sale and purchase transaction:

Buy-to-let and right-to-buy

Buy-to-let purchases and sales

If you are contemplating buying a property for the purpose of renting it out then you are looking at becoming a landlord of a ‘buy to let’ property.

Investing in Property has become very popular in recent years. Sydney Mitchell can assist you in navigating the legal complexities in purchasing a property as a buy to let investor either in your individual name or in the name of a company. Let our specialist conveyancers and solicitors guide you through every step of the process, whether that is a leasehold apartment or a freehold house.

Right-to-buy purchases

Right to Buy is a government scheme which enables most UK Council tenants, and some Housing Association tenants, to purchase their rented property at a discounted rate, based on the length of time they have occupied it.

It may be possible for you to apply to buy your home from the Council or Housing Association if it is your only or main residence and you are a secure tenant.

It is important to note that you will become fully responsible for the repair and maintenance of the property following your purchase of the property.

What is shared ownership and how does it work?

Shared ownership (also referred to as part buy part rent) is a low cost option that enables people to get their feet on the housing ladder. It’s particularly popular with first time buyers who haven’t been able to buy. There are a variety of different schemes available but in it’s simplest form ownership of the property is split between you and the housing association e-g on a 50-50 basis and you pay rent to the housing association on the share which you do not own.

Shared ownership for first time buyers

If you are a first time buyer, you will no doubt be aware of the large costs associated with purchasing your first property and getting yourself onto the property ladder. Shared ownership could provide you with an easier and more affordable route into home ownership.

Shared ownership mortgages

As you will only be purchasing a partial percentage of the property value, you will need to ensure that you seek out a mortgage compatible with shared ownership schemes at the best rate. Shared ownership mortgages are available from most mortgage lenders, however if you are considering shared ownership then you must seek independent financial advice in order to secure the best arrangement for you.

Frequently asked questions

Below are some frequently asked questions that our Residential Property team are asked in relation to the buying and selling of property.

What is Stamp Duty?

Stamp Duty Land Tax (SDLT) is a tax payable by the purchaser of residential or commercial land or property in England and Northern Ireland.

How much Stamp Duty Land Tax (SDLT) do I need to pay?

The amount of Stamp Duty Land Tax (SDLT) payable by a purchaser will depend on various factors, such as the purchase price of the property, whether the property being purchased is residential or commercial and whether any reliefs or exemptions are applicable.

A web link for the Government Stamp Duty Land Tax Calculator can be found here. Please follow this link and use the SDLT calculator to work out how much tax will be payable on your particular transaction.

Am I a First-Time Buyer for the purposes of Stamp Duty Land Tax (SDLT)?

When purchasing land or property, you will be considered a First-Time Buyer, and therefore able to claim First-Time Buyer’s Relief for Stamp Duty Land Tax purposes, if you satisfy the following criteria:

- You have never owned or had an interest in a property or land anywhere in the world. (This includes never having inherited or being gifted a property or land anywhere in the world)

- You must occupy the property being purchased as your main residence

- Your spouse or civil partner must also satisfy the criteria of a First-Time Buyer, whether purchasing the property jointly or in your sole name.

(HMRC treats married couples as a single entity for the purposes of Stamp Duty Land Tax)

What searches do I have to have and why?

Searches are carried out to find out information about the property you wish to purchase, and may include:

- Local search – this is designed to inform you of the planning history of the property and advise you of any housing development, as well as nearby road or rail schemes

- Land Registry search – this protects your interest in the property and ensures that no interest can be registered against the property before your ownership is registered.

- Drainage and Water search – this tells you where the adopted drains run close to your property. This can be useful if you wish to build an extension in the future. It will also confirm whether you are connected to the main sewers and water. It does not reveal private drains

- Environment search – this will tell you if your intended purchase is on a flood plain or contaminated land, or close to a landfill site.

It may be necessary to carry out additional searches dependant on where the property you are looking to purchase is situated. Your solicitor will advise you if any special searches are required.

Do I need to have a survey?

If you will be taking out a mortgage to fund your purchase you will be required to have a survey carried out on the property. If you are not having a mortgage whether you have a survey carried out is optional. However we would always recommend having a survey carried out to the property.

Can I pull out of the sale/purchase?

In England and Wales, the transaction does not become legally binding until you exchange contracts. Therefore you can stop the transaction at any point prior to this.

Be aware that if you do pull out you will lose any money that you have already spent on searches or surveys.

When do I pay the legal fees?

Conveyancing solicitors usually request an initial payment to cover the cost of searches and initial disbursements. The remainder will be requested from you following exchange of contacts but before completion.

What happens on completion day?

On the day of completion the buyer’s solicitors will transfer the purchase money to the seller’s solicitor via telegraphic transfer.

- It can take between one to six hours for the money to be received by the seller’s solicitors depending on processing times with the banking system

- The seller’s solicitor cannot authorise release the keys until the money has been received so this may not be until late afternoon

- Once the seller’s solicitors have received the money the buyer will be notified that they can collect the keys from the estate agents or from the seller depending on what has been agreed.

What are the key aspects of a right-to-buy purchase?

- Discounted purchase – Eligible tenants have the opportunity to purchase their property from the Council or Housing Association for less than the market value. The value of the discount available will increase the longer the individual has been a tenant

- Repayment clause – If you sell the property within five years of purchasing, you will most likely be required to repay some or all of the discount, the amount of which will be dependent upon on when you sell the property. For example, if you sell the property within 1 year of purchasing, you may be required to pay 100% of the discount, 80% in the second year, 60% in the third year, 40% in the fourth year and 20% in the fifth year

- Right of first refusal – Despite selling the property, the Council or Housing Association will retain a Right of First Refusal for the first 10 years following your purchase. This means that should you wish to sell or transfer the property within 10 years of purchasing it, you must obtain consent to do so from the Council or Housing Association, as they have the right to take back the property, should they wish to do. This rule applies to any subsequent owners wishing to sell the property within 10 years of it being purchased from the Council or Housing Association.

What is the process of purchasing a right to buy property?

To purchase a Right to Buy Property from the Council or Housing Association, the following steps must be followed:

- Check that you meet the eligibility criteria.

- Submit your application to the Council or Housing Association.

- Receive a formal offer with details of the valuation and discount, which you will need to either accept or decline.

- Proceed with the usual process of purchasing a property.

Should you wish to sell a property that you purchased as part of the Right to Buy scheme, Sydney Mitchell can also assist in this process.

Find out more about the team